Wars and Wall Street: Putting World News and Global Markets in Perspective

Whether reading the news or discussing investments in the first half of 2025, words like “fear” and “anxiety” have been heavily scattered throughout the vocabulary of newsreaders, investment professionals and the general public alike.

Locally, fears of loadshedding returning, the GNU collapsing, land expropriation without compensation and a second Great Trek (Afrikaners emigrating to the US as refugees) have dominated discussions around braais and boardroom tables. Yet despite the concern felt by many investors, and the flight to offshore investment opportunities, the Rand has steadily strengthened against the Dollar and the JSE has returned an outstanding 19,69% in a mere six months.

It could be argued that the average South African has become somewhat conditioned to stomach these uncertainties and is able to (in words used by Martin Luther King Jr.) “keep on keeping on,” knowing that the future is often not as dire as one initially fears. The developed world, on the other hand, in the absence of these regular worst-case-scenario fears, has been shaken by the storms of 2025. Yet the same truth remains… the future is often not as dire as one initially fears.

Let us, for a moment, take a glance in the rearview mirror and reflect on some of the headlines that drove public opinion in this strange new reality, where many investors spent more time looking at the newsfeeds of X (previously Twitter) and Truth Social than the fundamentals of investing.

January – February: Fear of an AI Bubble Burst

After another year of outstanding returns for the US market and technology stocks, many started to question the longevity of the euphoria surrounding US exceptionalism and investment in artificial intelligence. Many feared that the ever-increasing premium at which US and technology stocks traded above their intrinsic value and current earnings could be the writing on the wall for an AI bubble to burst.

With apprehension as the flavour of the month, talks of US tariffs on Canada and Mexico, as well as the launch of the Chinese AI model, DeepSeek, increased the unease felt by many. Market moves remained fairly subdued in this environment with the S&P 500 returning a mere 1,21% [USD] over the two-month period.

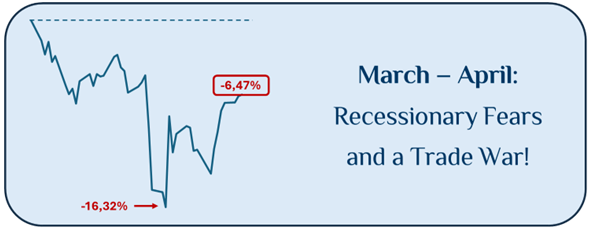

March – April: Recessionary Fears and a Trade War!

In March of 2025, recessionary fears were in full swing when, as if to add fuel to the fire, the announcement of the Liberation Day tariffs resulted in an already bruised market, experiencing a further loss of more than 10% over the subsequent two days. President Trump’s flip-flopping between policy implementation and the postponement thereof, in order to create opportunities for negotiations, caused severe volatility and uncertainty in global financial markets.

Over the two-month period, the S&P 500 incurred a loss of 6,47% [USD], although many anxious investors experienced far more extreme losses by being quick to sell positions and not partaking in the market recoveries upon policy reversals.

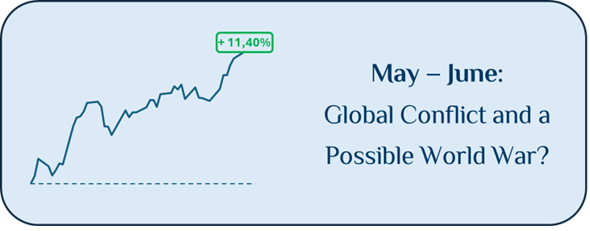

May – June: Global Conflict and a Possible World War?

While some form of normality returned to financial markets in May of 2025, as news of the Trade War was slowly replaced by news of trade agreements, geopolitical tension remained high. The prolonged war in Gaza divided nations as Israel expanded its military offensive in the district. The Russia-Ukraine War continued with confirmed reports of North Korean troops fighting alongside Russians. Israel’s surprise attack on Iranian military officials, scientists and the Islamic Republic’s nuclear program sent shots of terror as many feared the United States would be implicated or drawn into a conflict that would start World War III. Yet despite the US becoming directly involved, a ceasefire was negotiated a few days later, and the conflict was labelled the “12 Day War”.

One might presume that in such an environment chaos ensues in financial markets and investors experience extreme volatility and losses. Quite the contrary was in fact true. After waves of shocks and surprises as the world tried to negotiate the turbulent new waters of Trump politics and economics, a robustness had developed in financial markets. While many investors might have been on edge, they were equally reluctant to jump at an impulse, having already priced in an increased measure of uncertainty in their positioning. The S&P 500 was able to deliver an outstanding return of 11,40% [USD] over the two-month period despite the warnings of doomsday prophets.

A New Normal Requires a New Perspective

The global financial market has proven itself more durable than many feared at the start of the year, withstanding waves of onslaught. The unpredictability of politics and markets has resulted in short term trading on sentiment or extrapolated growth expectations becoming more akin to gambling where the pain of the loss often far outweighs the potential gain. Investors are increasingly positioning themselves to be able to stomach shocks and roll with some of the punches, while holding on to their longer-term investment thesis. Dare we say the cause for concern has initiated the return of sensible investing?

In many ways global markets have taken on a risk profile that we in South Africa are more accustomed to, where growth opportunities need to be pursued with a healthy respect for worst-case-scenario risks and a form of protection against these eventualities. Calculated, long-term investment decision making and effective risk management becomes cardinally important in such market conditions, where an emphasis needs to be placed on both capital protection and wealth multiplication.

Written by Kobus Jansen van Vuuren

{kind=link}